Blog Customer ServiceFintech Customer Service: The Modern Playbook

Fintech Customer Service: The Modern Playbook

Fintech customer service is its own discipline. Here's how modern teams handle high-stakes tickets, regulation, AI, and trust without losing the human touch.

✨ Automate your support with the fastest AI-enhanced Inbox today →

In fintech, every support ticket touches money. A frozen card affects rent today, not next quarter. A failed payout doesn't get resolved by "we're looking into it" - the customer is checking their account every five minutes until it lands.

This guide covers what makes fintech customer service different from generic SaaS support, the scenarios your team will actually handle, the best practices that earn trust, and the metrics worth measuring. 👇

Key takeaways:

- Fintech customer service is high-stakes by default. Every conversation touches a customer's money, time, and trust at once.

- Compliance and identity verification are first-class operational concerns, not afterthoughts bolted onto a generic support workflow.

- Most fintech support tickets cluster into a handful of recurring scenarios (fraud, chargebacks, KYC, failed payouts, lost cards), each with its own playbook.

- AI agents handle tier-1 well, but the wins go to teams that integrate AI deeply rather than bolt it on, with safe escalation paths to humans for anything compliance-touching.

- The metrics that matter aren't just response time and CSAT. Fintech teams also need to track verification success, escalation accuracy, and post-incident retention.

- Featurebase✨ is a modern AI-powered customer support platform that combines an omnichannel inbox, AI agents, and a help center into one place, designed for product-led teams that want the support side of fintech to feel as fast as the product side.

What is fintech customer service?

Fintech customer service is the support function for any product where money or sensitive financial data sits at the center of the customer experience: neobanks, payment processors, lending platforms, crypto wallets, embedded-finance providers, investing apps, and the long tail of B2B financial infrastructure.

What makes it distinct from generic SaaS support is that the consequences of an unresolved ticket are immediate and financial. A bug in a project-management tool is annoying. A bug in a payout flow means a small business can't make payroll.

Most fintechs run their support through some mix of three surfaces: in-app live chat or messenger, email, and a knowledge base or help center. Larger teams add phone, social, and sometimes a dedicated dispute-resolution portal.

Why fintech customer service is different from regular support

Three things separate fintech support from the rest of SaaS. They compound. Once you've worked through them, the rest of the operational decisions tend to follow.

The stakes are financial, not cosmetic

When someone contacts a fintech, it's almost never because they're mildly curious about a feature. It's because their money is doing something they didn't expect: stuck, missing, charged, frozen, or moved by someone who shouldn't have access.

J.D. Power's 2025 U.S. Direct Banking Satisfaction Study found that direct (digital-first) banks score 24 to 35 points higher on overall satisfaction than regional and national banks on a 1,000-point scale, largely because of digital-channel quality. The takeaway for fintechs: when there's no physical branch, the support experience IS the brand. There's nothing else for the customer to fall back on if it fails.

Every conversation lives inside a regulatory perimeter

A fintech support agent doesn't have the same conversational freedom a SaaS agent does. The wrong answer to a "why was my account frozen?" question can violate disclosure rules, tip off a fraudster about an open investigation, or commit the company to a chargeback decision it hasn't actually made.

Most of the consequential conversations are governed by some combination of KYC/AML rules, PCI-DSS, GDPR (or local equivalents), and product-specific frameworks like PSD2 in Europe or NACHA in the US. Agents have to know what they can say, what they can't, and what gets escalated.

That’s why teams often pair their support workflows with verification tools like Ondato to keep onboarding and identity checks compliant.

There's no branch to fall back on

Trust in fintech is high. 85% of consumers and 90% of small businesses report high levels of trust in fintech per the Financial Technology Association's 2025 State of Fintech survey. But that trust is held differently than trust in a bank with a building on the corner of your street.

A traditional bank customer who can't resolve an issue online can walk into a branch. A fintech customer who can't resolve an issue in the app has no fallback. That's why support latency and clarity hit harder in fintech. Every minute the issue is unresolved, the customer is sitting alone with their phone, watching their balance.

The support scenarios fintech teams actually handle

Most fintechs see the same handful of ticket types over and over. Building a playbook for each one (what the agent needs to verify, what they can and can't say, what gets escalated) is the single highest-leverage thing a fintech support lead can do.

Suspected fraud and account-lockout requests

These are the highest-pressure tickets you'll handle. A customer thinks their account is compromised, or your fraud system has frozen it for them. They want answers immediately. You can't give them the full picture because doing so could compromise an active fraud investigation or alert the actual fraudster (which, on a small but real percentage of tickets, might be them).

The playbook: verify the caller's identity through a separate channel from the one they're reaching out on (a known phone number, a registered-device push, biometric), acknowledge the freeze without explaining its cause, and route to the fraud team. The customer needs to feel heard. The agent needs to stay inside the disclosure rules.

Chargeback and dispute inquiries

Customers often think "I want to dispute this charge" is the start of a refund conversation. Legally and procedurally, it's the start of a regulated chargeback flow that involves card networks, evidence collection, and a fixed timeline.

The playbook: capture the dispute reason in the right code (Visa and Mastercard each have their own), gather supporting evidence, explain timelines plainly (most chargeback investigations take 30 to 90 days), and never promise an outcome you can't deliver. "I'll get that refunded for you today" is the most expensive sentence in fintech support.

KYC re-verification and identity proofs

Regulators require fintechs to periodically re-verify customer identity, especially after risk-flag events. Customers find these requests jarring. They signed up six months ago and now you want their passport again?

The playbook: explain why the re-verification is happening in plain language ("we're required to do this annually for accounts over a certain balance"), provide multiple submission paths (in-app upload, email, video verification), and don't let the account stay frozen longer than necessary once the documents land.

Payout delays and failed transactions

A payout that doesn't land is the ticket that ages the worst. Every minute it's open, the customer is more anxious and your support metrics get worse.

The playbook: have a transaction-status integration so agents can see exactly where the money is (initiated, in-flight, settled, returned), provide a realistic ETA based on the rail involved (ACH, RTP, SEPA all have different settlement windows), and proactively notify the customer when status changes. "I don't know where your money is" is unacceptable. "It's on its way, settles by 5pm tomorrow" is what trust looks like.

Lost or stolen card reports

Card replacement is procedurally simple but emotionally loaded. The customer is in a checkout line, at an airport, or filling up a tank, and the card doesn't work.

The playbook: freeze the card before anything else, surface a digital card immediately if the product supports it, and ship the physical replacement with realistic timing. If your product supports instant Apple Pay or Google Pay provisioning, this is the moment that earns lifetime loyalty.

Best practices for modern fintech customer support

Train for product, regulation, and cybersecurity together

Most fintech support training programs treat these as three separate modules. They shouldn't be. An agent dealing with a suspected fraud ticket is using product knowledge to understand the customer's account state, regulatory knowledge to stay inside disclosure rules, and cybersecurity knowledge to verify the caller isn't the fraudster.

Train them as one integrated practice. The scenarios from the previous section are the right training material, paired with general customer support skills like empathy, active listening, and de-escalation. Each one cross-cuts all three domains.

Verify identity before discussing anything

The first action on any account-touching conversation is identity verification. Not "after a couple of questions" - first.

Multi-factor verification is the bar:

- A registered-device check - push to a known device or biometric

- A second factor - security question, time-based code, or knowledge-based authentication

- A behavioral signal - login history, transaction patterns, geo-consistency

Verification has to be efficient enough that legitimate customers aren't punished for being legitimate. Three minutes of identity gymnastics for a "can I see my recent transactions?" question is its own bad experience.

Run one inbox across every channel

Fintech customers move between channels mid-issue. They start with a chat, escalate to email when the issue gets complex, and call when nothing's resolved. If your agents see those as three separate tickets, the customer is repeating themselves three times.

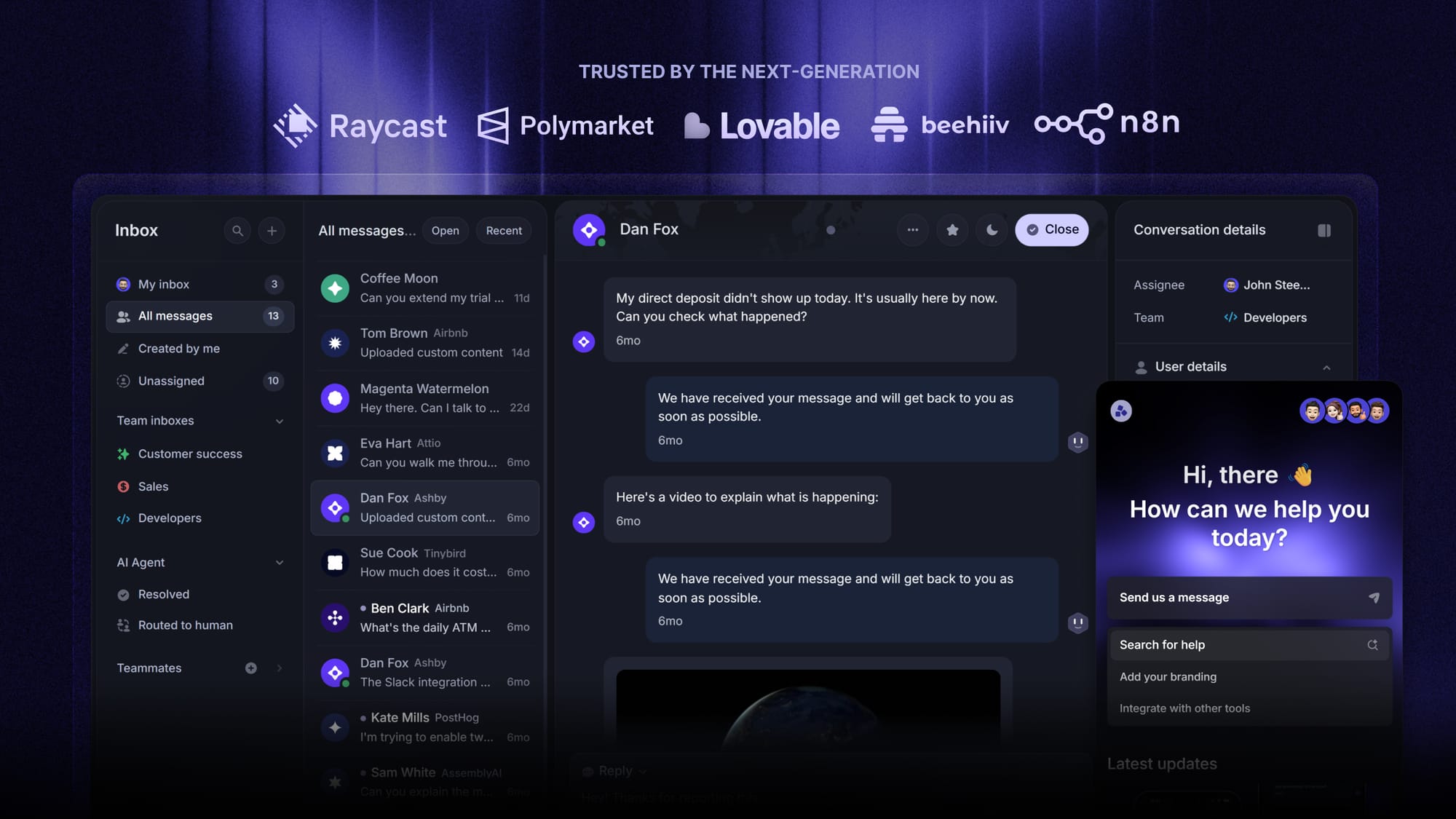

A unified inbox that aggregates live chat, email, and other channels into a single conversation thread, with full context, transaction history, and prior tickets visible, is the operational backbone of modern fintech support. With Featurebase you can route conversations from chat, email, and Slack into one AI-powered view, with the same agent seeing everything the customer has touched.

Deploy AI for tier-1 with safe handoff to humans

AI agents are now table stakes for tier-1 fintech support. Questions like "how do I reset my password," "where do I find my account number," "what's your routing number" don't need a human and shouldn't get one. Per Intercom's 2026 Customer Service Transformation Report, 82% of senior support leaders invested in AI for customer service over the past 12 months, but only 10% report mature deployment where AI is fully integrated into operations at scale. The wins are going to the teams that go deep, not the ones that bolt on a chatbot.

The handoff rules matter most in fintech. The AI agent has to know when to stop trying and route to a human, especially for anything that touches an account-state change, a fraud signal, a regulatory question, or a confused customer escalating in tone. Get the handoff right and you save your humans for the conversations that need them.

Close the loop between support and product

Support agents see the bug reports, the feature requests, and the trust-eroding edge cases first. Most fintech support tools don't have a real pipeline back to product. Issues get filed in a ticketing system and disappear.

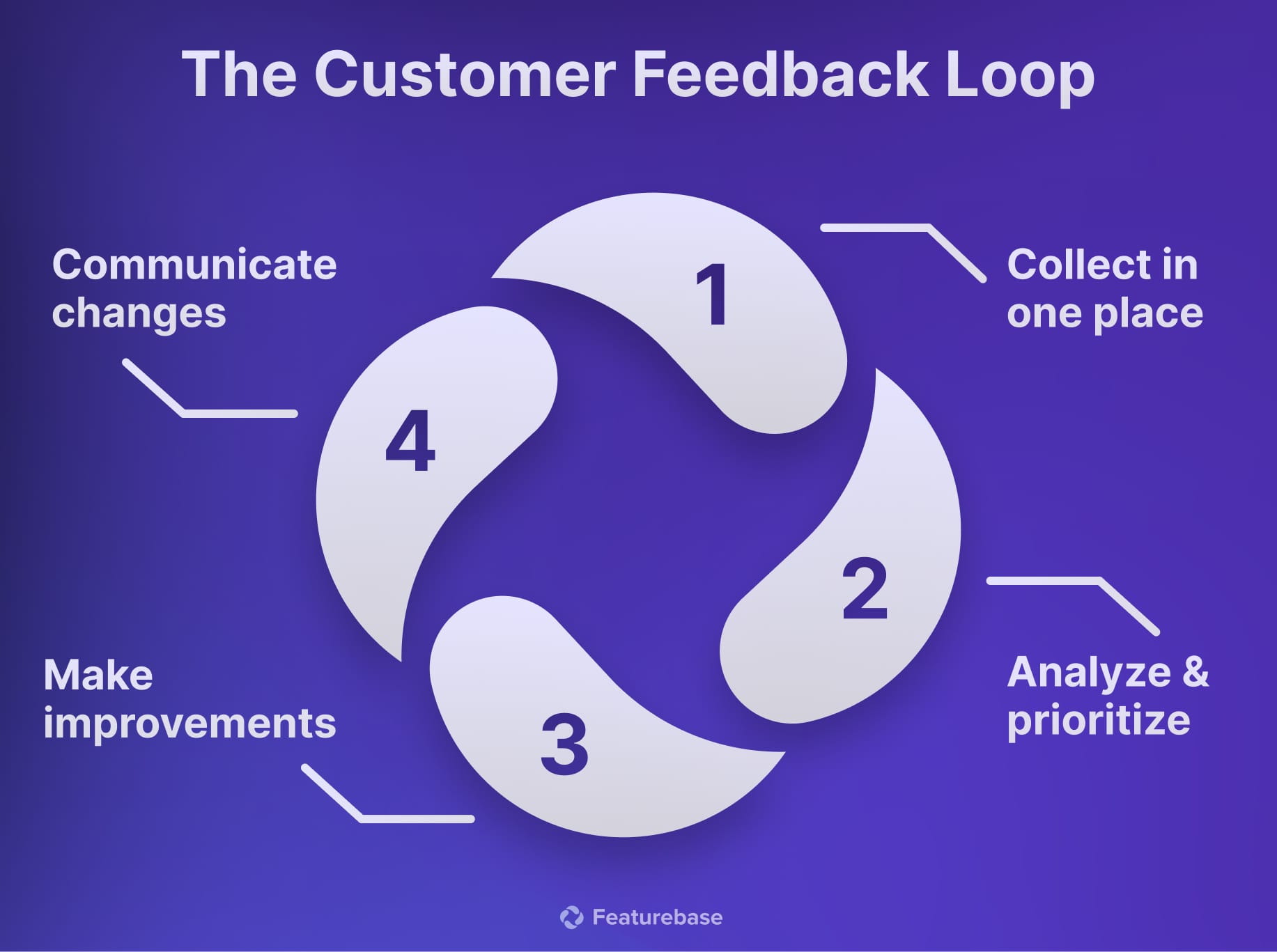

A modern setup connects support tickets to a feedback system the product team actually triages. Recurring complaints surface to a feedback board, and roadmap updates flow back to the customers who originally raised the issue. That's the customer feedback loop that turns fintech support into a growth signal rather than a cost center.

The metrics that matter most in fintech support

Standard support metrics still apply: first response time, resolution time, CSAT, deflection rate. But fintech has a few that the generic SaaS playbook misses:

- First-contact verification success: The rate at which an agent successfully verifies a customer's identity on the first attempt. Low numbers mean either fraud pressure (good, your controls are working) or excessive friction (bad, legitimate customers are getting stuck).

- Compliance-incident rate: Tickets where an agent said something they shouldn't have, missed a required disclosure, or breached a process rule. This number should approach zero through training plus regular QA.

- Escalation accuracy: When an AI agent or tier-1 human escalates, was the escalation correct? Over-escalation wastes senior time. Under-escalation lets risky tickets sit at the wrong level.

- Post-incident retention: When a customer hits a fraud event, a payout delay, or an outage, do they stay or churn? This is your real trust metric. CSAT measures whether the conversation was pleasant. Post-incident retention measures whether the conversation rebuilt trust.

Don't over-index on speed. A 30-second response that lands the wrong answer is worse than a 5-minute response that lands the right one - especially when the wrong answer carries regulatory or financial consequences.

Featurebase: A modern fintech-ready support platform

Featurebase is a modern AI customer support platform built for product-led teams that need the support side of fintech to feel as fast as the product side. It combines AI-powered support, help center, and feedback management into a single platform for startups that want all their customer-facing tools in one place. Featurebase is loved by thousands of support teams from companies like Lovable, Raycast, and n8n. 💫

Top features:

- Omnichannel inbox – Manage live chat, email, and Slack conversations from one AI-powered view

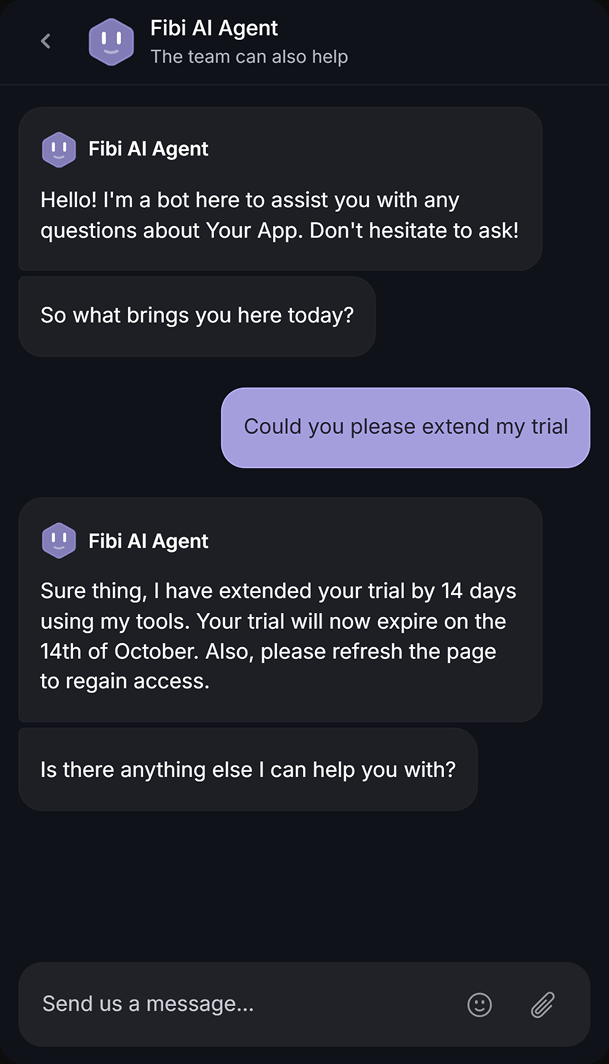

- Fibi AI Agent – Resolve customer issues on autopilot & run custom actions like trial extensions and refunds

- Help center with AI search – Provide instant, multilingual self-serve answers

- Workflows & automations – Auto-assign tickets, route conversations, collect customer data, and more

- AI Copilot – Help your agents answer customers faster with AI Copilot that uses your internal knowledge

- Multi-brand support – Manage multiple Help Centers and Live chats from a single workspace

- Automatic AI translations – Automatically translate all messages and help articles to your customers native language

- Service Level Agreements – Track SLAs to make sure your team responds to customers on time, every time

- Mobile app – Respond to customers, receive notifications, and unblock users on the go

- Feedback & roadmap tools – Collect feature requests and close the loop with updates

- Product updates – Publish release notes with a changelog page, in-app widget, and emails

- Integrations – Connects with Slack, Linear, Jira, HubSpot, and more

Pricing: Free plan available with unlimited conversations. Paid plans start at $29/seat/month with $0.29 per AI resolution.

Featurebase covers all the basic support features that legacy platforms do, but with a much more modern approach. It comes with AI automations, a mobile app, and multiple channels (email, live chat, Slack, etc.).

Resolve fintech support faster

Manage chat, email, Slack, AI answers, and human handoffs from one support inbox.

Conclusion

Fintech customer service is its own discipline. It's not generic SaaS support with a compliance overlay. It's a different operational model where every ticket carries financial weight, every channel is regulated, and every minute the issue stays unresolved is a minute the customer is alone with their money.

The teams that win treat each piece as a first-class concern: a real scenario playbook, identity verification before any account discussion, an inbox that aggregates every channel into one view, AI deployed deeply enough to handle tier-1 with safe escalation, and a feedback loop back to product so issues stop recurring.

Featurebase is a modern AI-powered customer support platform built for teams that need the support experience to match the product experience. It combines an omnichannel inbox, AI agents, a help center, and feedback management into one platform, so fintech support stops being a cost center and starts being a trust engine.

It comes with a Free plan with unlimited conversations, and the onboarding is incredibly quick, so there's no downside to trying it out. 👇

✨ Automate your support with the fastest AI-enhanced Inbox today →

FAQs

What makes fintech customer service different from traditional banking?

Traditional banks have branch networks customers can walk into when something breaks. Fintechs don't, which means support is the entire fallback layer. Add the regulatory weight on every conversation (KYC, AML, disclosure rules) and the stakes on every ticket, and you get a different operational discipline. Same goal as banking support, but a different operating model to deliver it.

What KPIs should fintech support teams track?

The SaaS basics still apply: first response time, resolution time, CSAT, and deflection rate. Fintech teams also need fintech-specific signals like first-contact verification success rate, compliance-incident rate, escalation accuracy, and post-incident retention. The last one is the closest thing to a real trust metric: when a customer hits a fraud event or outage, do they stay or churn?

How can fintech startups scale support with a small team?

Lean on AI for tier-1 deflection and a strong self-service help center, then keep your humans for the conversations that actually need a human (fraud, disputes, account-state changes, anything compliance-touching). A modern setup like Featurebase puts an AI agent, an omnichannel inbox, and a help center on one platform, so a small team can cover everything a typical fintech account-holder would ask without burning out.

Should fintech customer support be in-house or outsourced?

In-house wins on compliance, product knowledge, and trust signals. Outsourcing can work, but only with rigorous training, regular QA audits, and clear escalation paths back to your in-house team for anything sensitive. Most growth-stage fintechs end up with a hybrid model: outsourced tier-1 for volume-driven channels, in-house for anything that touches regulation or account state.

How should fintech support teams handle outages and downtime?

Get ahead of the customer. The moment you confirm an outage, post status updates proactively across your status page, in-app banners, and email - silence is what destroys trust during downtime. Agents should use scripted reassurance language that's been compliance-reviewed, and once the incident clears, send a follow-up explaining what happened and what you're doing about it. Customers forgive outages they understand.

How do fintech support teams stay compliant during conversations?

Identity verification before any account-specific discussion is the baseline. Never make exceptions, even for legitimate-sounding customers. From there, agents need scripted disclosures for the regulated moments (chargebacks, fraud flags, account closures), encrypted channels for any sensitive data exchange, and role-based access so they only see the information they need for that ticket type. Quarterly compliance training keeps the rules fresh as regulations evolve.